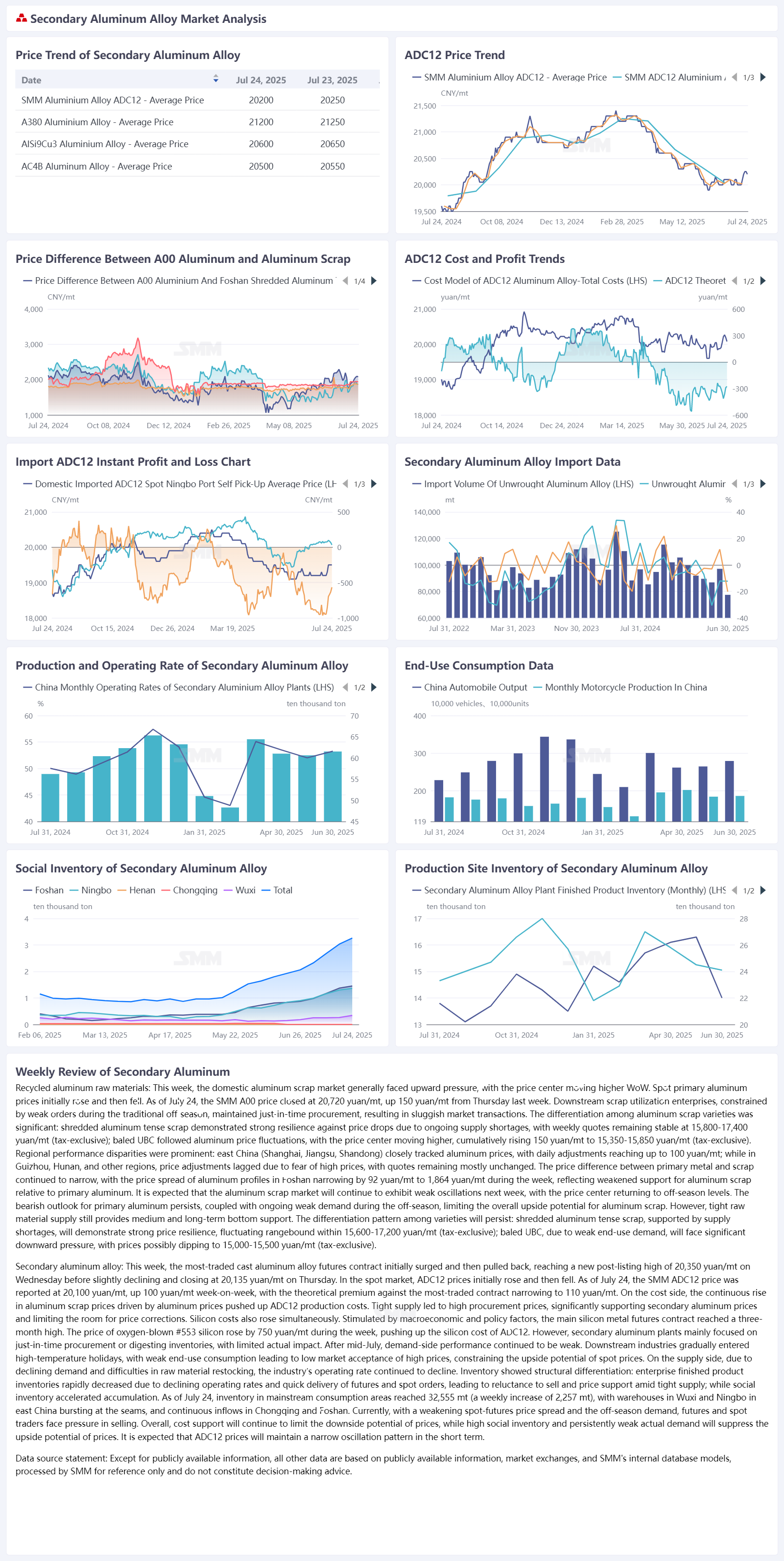

Aluminum Scrap: This week, the domestic aluminum scrap market generally faced upward pressure, with the price center moving higher WoW. Spot primary aluminum prices initially rose and then fell. As of July 24, the SMM A00 price closed at 20,720 yuan/mt, up 150 yuan/mt from Thursday last week. Downstream scrap utilization enterprises, constrained by weak orders during the traditional off-season, maintained just-in-time procurement, resulting in sluggish market transactions. There was significant differentiation among aluminum scrap varieties: shredded aluminum tense scrap demonstrated strong resilience against price drops due to ongoing supply shortages, with weekly quotes remaining stable at 15,800-17,400 yuan/mt (tax-exclusive); baled UBC followed aluminum price fluctuations, with the price center moving higher, cumulatively rising 150 yuan/mt to 15,350-15,850 yuan/mt (tax-exclusive). Regional performance differences were prominent: east China (Shanghai, Jiangsu, Shandong) closely tracked aluminum prices, with daily adjustments reaching up to 100 yuan/mt; while in Guizhou, Hunan, and other places, price adjustments lagged due to fear of high prices, with quotes mostly remaining flat. The price difference between primary metal and scrap continued to narrow, with the price spread of aluminum profiles in Foshan narrowing by 92 yuan/mt to 1,864 yuan/mt during the week, reflecting weakened support for aluminum scrap relative to primary aluminum. It is expected that the aluminum scrap market will continue to be in a weak oscillatory pattern next week, with the price center returning to off-season levels. The bearish outlook for primary aluminum has not dissipated, coupled with the continued suppression of weak off-season demand, limiting the overall upside potential for aluminum scrap. However, the tight supply of raw materials still provides medium and long-term bottom support. The differentiation pattern among varieties will continue: shredded aluminum tense scrap, supported by supply shortages, will demonstrate strong price resilience, fluctuating rangebound within 15,600-17,200 yuan/mt (tax-exclusive); baled UBC, due to weak end-use demand, will face significant downward pressure, with prices possibly dropping to 15,000-15,500 yuan/mt (tax-exclusive).

Secondary Aluminum Alloy: This week, the most-traded contract of cast aluminum alloy futures initially jumped and then pulled back, reaching a new post-listing high of 20,350 yuan/mt on Wednesday before slightly declining, closing at 20,135 yuan/mt on Thursday. On the spot market, ADC12 prices initially rose and then fell. As of July 24, the SMM ADC12 price was reported at 20,100 yuan/mt, up 100 yuan/mt WoW, with the theoretical premium against the most-traded contract narrowing to 110 yuan/mt. On the cost side, the continuous rise in aluminum prices drove up the production cost of ADC12 due to the increase in aluminum scrap prices. Tight supply led to high procurement prices, significantly supporting secondary aluminum prices and limiting the room for price corrections. Silicon costs also rose simultaneously. Stimulated by macroeconomic and policy factors, the main contract of silicon metal futures reached a three-month high. The price of oxygen-blown #553 silicon rose by 750 yuan/mt WoW, pushing up the silicon cost of ADC12. However, secondary aluminum plants mainly focused on just-in-time procurement or digesting inventories, resulting in limited actual impact. After mid-July, demand-side performance continued to be weak. Downstream industries gradually entered high-temperature holidays, and weak end-use consumption led to low market acceptance of high prices, constraining the upside potential of spot prices. On the supply side, due to declining demand and difficulties in raw material restocking, the industry's operating rate continued to decline. Inventory showed structural differentiation: enterprise finished product inventories rapidly decreased due to reduced operating rates and quick delivery of futures and spot orders, leading to reluctance to budge on prices amid tight supply; while social inventory accelerated its accumulation, reaching 32,555 tons (a weekly increase of 2,257 tons) in major consumption areas on July 24. Warehouses in Wuxi and Ningbo in east China were full, with continuous inflows in Chongqing and Foshan. The current weakening of the spot-futures price spread, coupled with the off-season demand, put pressure on futures and spot traders to sell. Overall, cost support will continue to limit the downside potential of prices, while high social inventory and persistently weak actual demand will suppress the upside potential of prices. It is expected that the ADC12 price will maintain a narrow oscillatory pattern in the short term.

![2026 Arrangements for Secondary Aluminum Alloy Enterprises During Chinese New Year Break [SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)

![Costs Drag Down Supply-Demand Pressure, Aluminum Auxiliary Material Prices Under Pressure and Weaken [SMM Analysis]](https://imgqn.smm.cn/usercenter/NQyKF20251217171655.jpg)